Rising demand for electric vehicles and supply challenges because of the Ukraine War are impacting the sector, says head of Motor Sector at Bank of Ireland Stephen Healy.

“The sector worked through the pandemic and has suffered supply shortages at a point when demand soared”

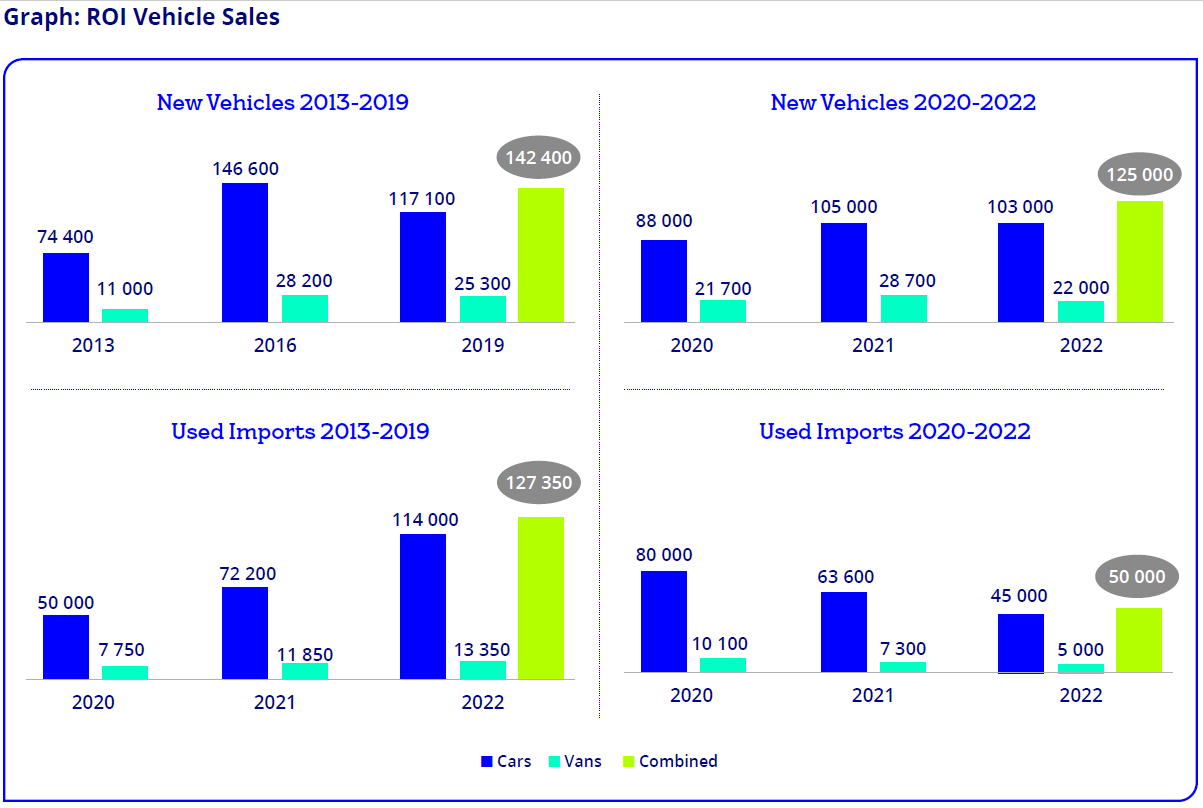

2021: Brief lookback

Lest we forget, Level 5 COVID restrictions were in place for the first 4.5 months of 2021. Motor dealers continued to open for vehicle aftersales, an essential service, and consumers could visit dealers to have maintenance carried out.

For vehicle sales, dealers engaged with customers remotely and operated a “click and deliver” service. By the end of H1 2021, combined sales of new cars and vans were ahead 27% compared to H1 2020 and 16% behind H1 2019. International travel resumed in July 2021 and rental car companies began to increase their fl again. The hire drive channel accounted for just under 8% of new car registrations in 2021 (v. 3% in 2020).

New vehicle supply issues, caused by global supply chain challenges, started to bite in the second half of 2021. By year end, new passenger car registrations increased almost 19% year on year to 105k units.

Compared to pre-pandemic levels, new car sales were circa 10% lower than the 117k units sold in 2019. Light commercial vehicle registrations (LCV) increased by circa 32% year on year to just under 29k units. There were more new vans sold in 2021 than in the peak year of 2016 and highlights strong demand for commercial vehicles throughout the pandemic.

2022: The supply story

Pent up demand carried over into 2022, however, supply shortages have impacted the true market potential this year. This is due to continued global supply chain challenges and microchip shortages in the sector, impacting manufacturing output.

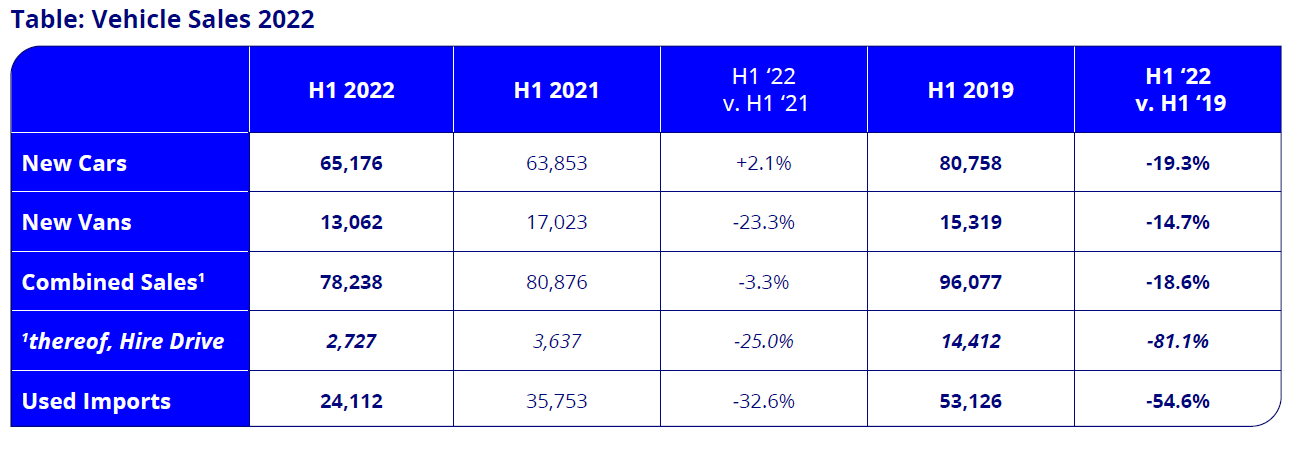

New car sales in Ireland increased 2% in H1 2022 but compares favourably to a decline of 11.9% in the UK and a decline of 14.0% overall in the EU. European sales in June 2022 were the lowest recorded since 1996. Back to Ireland, where new van sales declined 23% resulting in an overall market decline here of 3% in H1 2022.

Car rental companies are experiencing a material improvement in both revenue and income in 2022 following a torrid couple of years. They are struggling, however, to replace short term rental fleets.With new vehicles in short supply, motor franchises are concentrating supply into the retail sales channel which, generally speaking, is more profitable. The hire drive channel accounted for circa 4% of new car registrations in H1 2022 (v. 15% historic average). The supply shortage has led to increased car rental prices in Ireland, and across Europe, a trend widely covered in the media.

Used vehicles

Used cars are also in short supply due to lower new car sales in 2020 and 2021, increased vehicle registration tax (VRT) – which impacts affordability and demand – and reduced volumes of used imports due to Brexit. Residual values strengthened again in the first half of 2022 however, anecdotally, motor dealers report values have levelled off

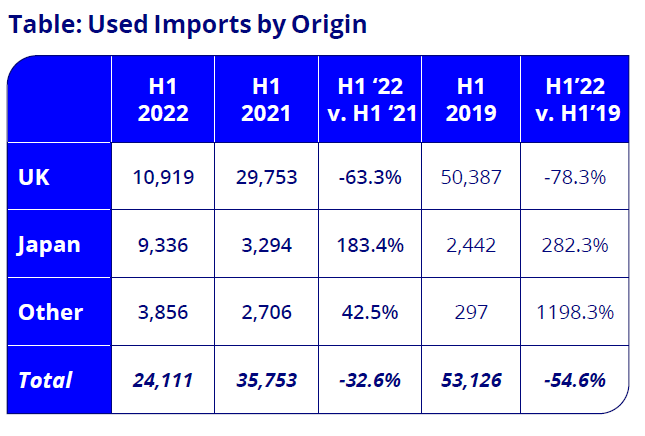

95% of used imported cars were sourced from the UK pre-Brexit. Dealers continue to import used vehicles where value is present, however rising residual values in the UK and tighter supply there have significantly impacted volumes imported to Ireland. Post Brexit, used car imports declined almost 21% in 2021 and were 44% lower than the peak in 2019. This refl the impact of Brexit, changes to VRT for used imports and tightened supply in the UK.

In H1 2022, used car imports declined by circa 33% year on year compounding a shortage of used cars in the market. The volume of used cars imported from the UK declined 63% (-78% from peak year) now representing just 45% of overall used imports. Dealers sought alternative sources to maintain supply and imports from Japan have increased notably. Japanese used imports have almost tripled by volume year on year and their share has increased to circa 40% of used car imports in the first half of 2022.

Ukraine

War in Ukraine has impacted automotive manufacturers in the form of disruption to supply chains resulting in reduced production capacity. Parts supply sourced by vehicle manufacturers from Ukraine was disrupted immediately following the outbreak of war and was particularly acute with regard to wiring harnesses. Some transport routes and financial transactions with Russia are impacted. Where possible automotive manufacturers have sourced parts from alternative suppliers, however this takes time to ramp up and delays compound vehicle inventories already at all-time lows.

Wiring systems supplier Leoni, operating in 28 countries employing circa 100k staff globally, is reported to have retained 90% of its 7,000 workforce in Ukraine and has returned Ukraine production to near pre-war levels. There are two plants based in Kolomyia (close to Romanian border) and Nezhukhiv (close to Lviv/Polish border) both in Western Ukraine. Following the outbreak of war, Leoni initially sent all staff home and off them alternative employment in its factories in Romania. Its staff however, largely wanted to remain in Ukraine. Astonishingly, operations continue amid repeated air raids alerts when staff need to take cover in bomb shelters….

Ukraine is a global supplier of Neon gas, used in the production of microchips. Several large chip producers, however, have reported diversification of supply chains post the annexation of Crimea, thus reducing their supply risk. Nonetheless the war exacerbates a pre-existing shortage and, although the outlook is for improved chip supply from H2 2022, microchip shortages will continue in the near term. A slowdown in demand for consumer electronics may free up much needed supply to the automotive sector.

Commodity prices and the cost of energy are heavily impacted. Input costs for manufacturers have risen substantially including general metals, aluminium, palladium (used in catalytic converters) and nickel ore (used in lithium-ion batteries).

The war is also having a profound impact on the motor sector in Russia. New vehicle sales plunged 84% in May, following a 78% slump in April. Russian car prices increased by about 50% this year, eroding demand, while sanctions have cut supply. 18 of 20 motor manufacturing plants have closed highlighting Russia’s dependence on Western brands. Just two plants remain open, one is local the other Chinese.

From an Irish perspective, disruption in automotive vehicle production has led to longer lead times for consumers here. Vehicle prices may rise in the near term as input costs continue to be elevated for vehicle manufacturers. Tesla has publicly commented higher input costs have led to increased Tesla prices this year.

Budget 2023

The last two government Budgets brought about sweeping vehicle registration tax (VRT) changes, ultimately leading to price increases for Irish consumers.

Encouragingly, VRT relief for battery electric vehicles (BEV) was extended in Budget 2022 for an additional two years to the end of December 2023. The SEAI purchase grant for BEV’s also continues. The SEAI purchase grant for plug-in hybrid vehicles (PHEV) was discontinued on 31/12/2021 and no further reliefs are available for these models. The Irish government is not unique in this approach. More governments across Europe are discontinuing PHEV incentives and are focusing incentives on BEV’s. So, what will happen in Budget 2023?

This remains to be seen. VRT increases brought about by the Minister over the last two years provides an insight into government direction and future policy changes. The motor sector was vocal in expressing its disappointment and frustration with recent VRT changes arguing strongly that increased retail prices will hamper growth in new car sales and the goal to remove older more polluting cars from our roads.

I can think of no other sector that experienced tax increases of this manner in the last two years, as the sector attempts to recover from the impact of the pandemic, shortages of supply and now war in Europe. In the face of unprecedented inflation one would hope the sector is due a reprieve in Budget 2023.

Electric car demand accelerating

Consumers are adopting new technologies at a faster pace each year as manufacturers design and roll out new low and zero emission vehicles. As recently as 2015, the combined share of electric vehicles and hybrids was less than 2% of new car sales in Ireland. By 2021, this share had increased to 34%.

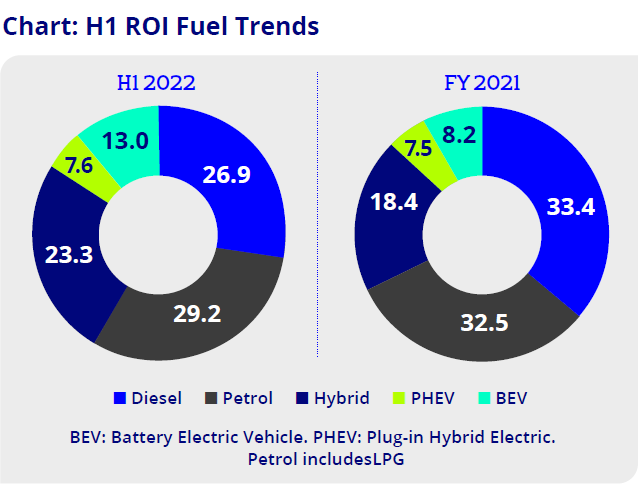

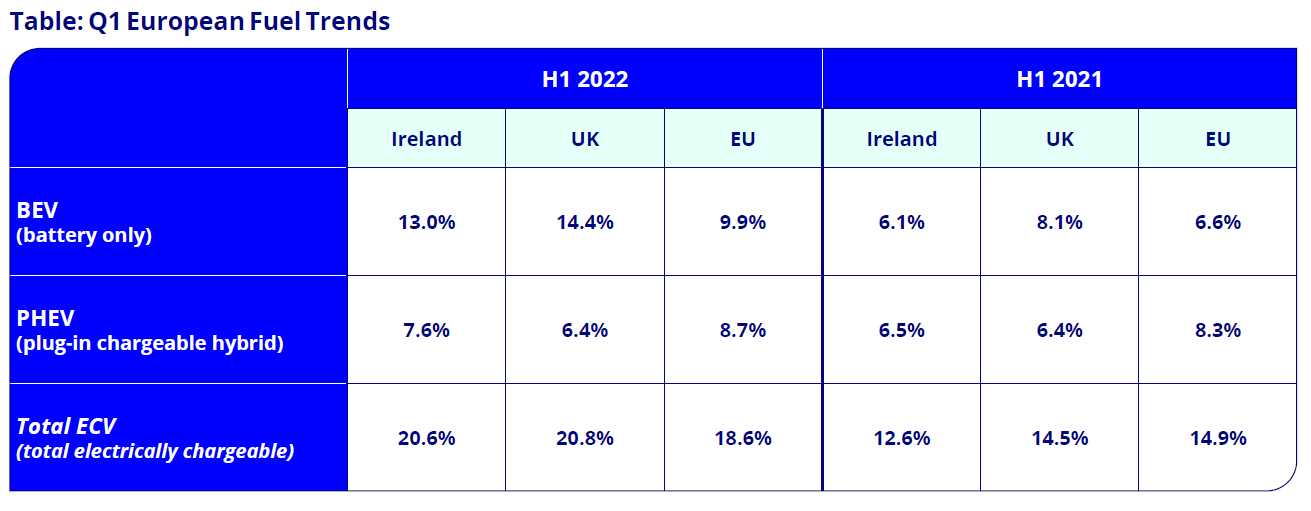

The take up of electric vehicles further accelerated this year with the combined share of electrically chargeable vehicles (ECV = BEV+ PHEV i.e. those with a plug attached) representing 20.6% of new car sales in H1 2022.

Combined sales of ECVs and Hybrids (non-plugged versions) now account for almost 44% of new cars registered this year. The share of diesel cars has fallen each year since 2015, however its popularity remains strong in Ireland with almost 27% buying diesel this year (well down from 70%+ peak). In the UK, for example, new diesel sales account for just under 6% of sales in H1 2022. Sales of ECV’s also ticked up across the EU in the first half of 2022.

Market growth needed

The Irish Government published the Climate Bill and refreshed the Climate Action Plan (CAP) in Q4 2021. In the latest CAP, the 2030 target for electric cars was increased to 845,000. An additional target of 95,000 has been set for electric vans. There are circa 50,000 electric vehicles on our roads today from a total of 2.2m passenger cars – we have quite a way to travel yet. For more detail on EV targets, reducing emissions and vehicle charging infrastructure, have a read of our last publication here.

In order to achieve electric vehicle targets set out in the latest CAP, the new car market simply needs to grow. The state can support the transition by continuing grants and incentives to accelerate BEV sales. This helps bridge the price gap until prices of BEV’s align with the internal combustion engine (ICE). Generally, the sector expects that BEV prices will align with ICE vehicles closer to the end of this decade. Government supports are vital to support the continued growth of electric vehicles in Ireland.

In the meantime, the sector continues its transition offering greater choice of new low and zero emission vehicles. New cars with petrol, diesel and hybrid engines will be sold alongside electric vehicles until at least the end of this decade.

Outlook

We are cautiously optimistic with regard to our outlook for this important sector in Ireland. In 2021 new car retail sales were almost on a par with 2019 levels if we exclude the hire drive sales channel. The sector worked through the pandemic and has suffered supply shortages at a point when demand soared. New car sales increased 2% in the first half this year, however, new car sales dipped circa 17% in July leading to a year on year decline of 3.6% in the first 7 months. This is caused by supply side constraints rather than weak demand.

We now operate in an inflationary environment and the uncertainty it brings. Despite the doomsayers (who may eventually be right) there are still positive nuggets to be found in a sea of uncertainty. We have almost full employment in Ireland. That is an extraordinary achievement following a pandemic unseen for 100 years. Of course, it brings its own challenges with regard to labour shortages, but let’s focus on the positives. Savings are at an all-time high. Interest rates will rise but off a low base.

Economists are still predicting growth in Ireland, and in Europe, in 2022 and in 2023 albeit pared back from previous expectations, but growth nonetheless. Per a recent Davy broker update, if Irish GDP were flat through Q2-Q4, calendar year GDP growth in 2022 would still equal 7.5%. If we are to believe economists, all things considered equal, inflation will start normalize mid-2023. At time of writing, commodity prices are starting to soften.

Demand for electric vehicles continues to rise and ECV sales will be circa 20% of new car sales in 2022 and will continue to rise next year. New van supply was severely curtailed this year and some manufacturers have had to delay new product launches in 2022 until 2023.

Generally speaking, new vehicle supply is expected to improve in H2 2022 for delivery in 2023. This is due to an expected supply increase already baked in for H2 and an expectation that an anticipated slowdown in demand for consumer electronics will feed much needed microchips back into vehicle manufacturers. They will be needed. Electric vehicles require far more microchips than internal combustion vehicles, so we can expect automotive manufacturers to take the increased supply.

There are always headwinds. Inflation is concerning and its potential impact to consumer sentiment. If Russia turns off their gas supply to Europe, this is likely to have an impact to European vehicle manufacturing and supply. Vehicle production plants are, however, spread globally and European manufacturers with the benefit of their own power stations may revert to using coal to ensure continuity of production.

Used cars will remain in short supply in the near term as there are not many avenues open to dealers to source stock. The new car market will need to grow to generate more new cars and therefore, used cars in the market. The sector could do without further VRT increases in the next Budget that will only serve to fuel inflation and slow the rate of ECV adoption.

This year, the new car market is unlikely to exceed 103k units due to supply shortages. That’s about 88% of 2019 pre-pandemic levels. It takes time to recover from recent extraordinary shock events. It’s early to call the market in 2023, however, we will provide updates in our monthly motor newsletters in the Autumn. In the meantime, it’s important to remember those positive nuggets.