More cloud investment is on the horizon for Irish business and consolidation is underway in the Irish tech sector, forecasts Bank of Ireland head of Tech, Media and Telecoms Paul Swift.

“The pandemic has not gone away, but lessons learned during this period are shaping how we live and work today and into the future. The physical work environment is being replaced by digital infrastructure, enabling businesses to become more productive, while working asynchronously”

TMT 2022 H1 Review

Summary

Technology

Over the course of the first half of the year there has been a marked uplift in activity as digitalisation continues. Businesses from every sector look to their IT services provider to deliver appropriate technology applications and solutions to help them continue on their transformation journey to meet the ever-changing needs of customers in a post-pandemic environment.

Media

Ireland’s screen/creative sector continues to go from strength to strength. During H1, Screen Ireland published its annual report for 2021 that posted record-breaking, screen industry production activity figures of €500 million (Screen Ireland) spent in the Irish economy. There was increased production growth in local feature film, TV drama and local animation. According to Screen Ireland, the level of spend on jobs, local goods and services was the highest ever achieved.

Telecoms

We are seeing a repeat of the trend of recent years where there is further consolidation in the sector. Telecoms providers are continuing to vertically integrate and acquire technology service providers to provide a ‘one-stop-shop’, delivering both connectivity and layering on other services to their customers, such as data storage and management, cyber protection and cloud services. In this way the service providers are becoming more embedded with their customers, increasing revenue while reducing customer acquisition costs.

H1 2022 Key Trends

Climate action: As the sustainability movement gains momentum and becomes a focus for everyone, citizens and businesses alike are looking for ways to reduce their carbon footprint. Technology is now seen as having a critical role to play in addressing climate action goals. There is increasing use of robotics, seen as a necessity for many industries struggling with labour shortages, which is more pronounced in some sectors than others. One of the benefits of cloud technology too, is that it reduces the need for companies to host their data on site, removing the cost of cooling large in-house hardware. Remote working is also supported through internet connectivity, which is also reducing the amount of people on the roads. These are just some examples and over time, as smart homes become more commonplace, citizens will have more power to manage domestic energy consumption, reinforcing the growing evidence of the role technology solutions will play in helping the environment.

Buy and build: Continuing the trend of recent years, we are seeing more businesses in the sector adopting a ‘buy and build’ strategy, targeting in some cases, ‘lifestyle’ businesses (where it is supporting the founder’s personal income, rather than maximising revenue); to help grow both revenue and customers locally and internationally. Many companies that have chosen this approach see it as an opportunity to augment their current technology suite with additional capabilities and skills or expertise or acquire a similar business in a different location and leverage synergies and seek to cross-sell and upsell.

Customer experience: Consumer behaviour is constantly changing and anytime, anywhere, any device is now expected, if not demanded, by customers. The simplicity of being able to swipe to conclude a purchase, is filtering down into people’s everyday expectations of what the customer experience should be. Competition is driving innovation. This doesn’t always mean having to build a technology platform from the ground up, rather customers now expect to see their service provider utilising devices or applications to enhance the experience. For example, when consumers are purchasing furniture or large household items, it is now expected the retailer uses modern technology to present what the item will look like in their home using augmented reality. These and other similar solutions are widely available in an application format. They can add value for businesses across all sectors that may not have the capacity to implement an entire omni-channel solution.

H1 2022 Key Activity in the Sector

Forecast is for more cloud

There is continued migration to cloud computing as more and more businesses are seeing the value in the scalability, agility, flexibility and accessibility the technology offers. According to Gartner, global investment in cloud services is forecast to grow 20.4% in 2022 to a total of $494.7 billion (Gartner) and expected to reach $600 billion in 2023. According to a recent survey carried out on C-level executives in Ireland, 81% (Deloitte ‘Looking to the clouds’ – March 2022) said it reduced costs, improved business resilience and quality of services, while on the other hand 78% of businesses stated that executive support and a lack of skills or resources are some of the barriers to adoption. Surprisingly, based on those results it could suggest that cloud service providers need to help businesses better understand the benefits and mitigate the risk that exists in relation to the adoption and integration of cloud computing technology, influencing the opinions of senior business leaders.

Need for continued vigilance against cyber-threats

Cyber threats are continuing to impact individuals, businesses and organisations everywhere. 39% (Hiscox Press Release Cyber Readiness Report 2021 – May 2022) of Irish companies suffered a cyber-attack in the past 12 months. Alarmingly 70% of those companies were targeted more than once. Phishing emails continues to be the main access point for fraudsters with smaller companies being the most likely victims. Ransomware is also very common; of those attacked, 75% paid the ransom. These findings, while shocking, should ensure there is an enhanced state of awareness across organisations everywhere and that no business should be complacent enough to think they will never be a victim. Despite the perception that these fraudsters are very sophisticated in how they perpetrate attacks, in reality they gain access to an organisation’s network and systems simply by someone unwittingly clicking on a link. The advice for all businesses is to always be vigilant.

Hollywood comes to Mullingar

Ireland’s reputation as a global location for the screen industry continues to rise and is now one of the foremost centres of excellence in animation and live action production globally. The boom in live action production and the worldwide demand for content is providing the incentive for investors to support the creation of more live studios. The latest of which was the announcement that a new studio has received planning approval in Mullingar. Hammerlake Studios (Hammerlake Studios Press Release – July 2022) looks set to create Ireland’s largest film studio, with a purpose-built film, television and content production campus constructed on a 25-acre site in Mullingar, Co Westmeath. This latest announcement comes on the back of expansions in studio space at Ardmore Studios (Wicklow), Troy Studios (Limerick City) and Ashford Studios (Wicklow) and the creation of new studios at Ashbourne and Greystones.

Lending activity

Our customers continue to reap the benefits brought about by the acceleration of digital over the last several years. Many technology providers that we have spoken to have told us that their relationship with their customers and clients has changed somewhat as a result, moving from a transactional to more of a partnership. Customers are in many cases still continuing to try and figure out what technology solutions can enable them to work smarter and more sustainably with their employees, suppliers and clients. This is where the partnership approach is helping solve these problems and solidifying the relationship, which is having in many cases a positive impact in growing revenues.

While we have seen an increase in the availability of capital from non-bank lenders over recent years, we are now also seeing an increase in demand from businesses seeking to refinance that funding over the first half of the year.

Sector Developments

New Seed and Early-Stage Fund launched

In April, there was good news for seed and early-stage technology companies with the announcement that Dublin-based Delta Partners had launched its new venture capital fund which will invest into seed and early-stage technology businesses in Ireland. The fund aims to invest in 30+ start-ups over the next three to four years at both seed stage and Series A. Bank of Ireland and Enterprise Ireland are cornerstone investors in this new fund along with Fexco and several family offices. Delta Partners also plan to attract other investors over the remainder of the year to reach target funding of €70 million. It has been well documented over recent years that there was a dearth of funding for early-stage companies and this new fund will hopefully go some way to plugging the gap. One of the first recipients of funding is Cork-based VisionR which received €1.5m in backing (from Delta Partners and Movidius co-founder Seán Mitchell). Their solutions aim to help bricks and mortar retailers personalise the customer journey and provide the retailer with the same level of insights their store would get if it was online.

Viatel continues its acquisition journey

Interesting to see Viatel continue on their acquisition journey across the first half of this year. Fresh from completing several transactions in 2021, they have continued on the same track with the completion of the acquisition of ActionPoint based in Limerick in January and followed it up with their most recent acquisition of SupportIT based in Dublin. This is the seventh acquisition for Viatel in two years and has expanded the breadth of their solutions from being a telco provider to now being a broad-based digital services group providing solutions for customers in connectivity, managed services, cloud and software development. This further demonstrates how the lines are continuing to blur across traditional sector boundaries where a telco now becomes a technology company and vice versa.

Grow Digital Fund Launched

The government recently announced a new €85 million fund to help businesses to go digital. This fund is open to any business from any sector and at any stage of their lifecycle. The first tranche of funding of €10 million is available in 2022 and will be administered through Enterprise Ireland. The objective of the fund is to get businesses to use digital tools, incorporating emerging technologies into their businesses with a view to assisting those businesses to embrace the potential of exporting their goods and services if they don’t already do so. This fund is welcomed and will help those businesses that may not know where to start on their digital journey, to take the first step, access support funding and begin.

Micro credentials helping meet the digital skills shortage

Micro credentials are small, or sometimes referred to as ‘bite-size’, accredited courses created to meet the demands of individuals, organisations and enterprise. They are becoming more commonplace now among Ireland’s learning institutions as they grapple to meet the actual learning needs of students, so they can quickly assimilate into evolving job roles and enhance employability of candidates. These types of courses are accredited/certified, flexible and typically delivered online. The big advantage of these courses is that they have the potential to offer education to those that may not otherwise be able to access these courses or those that cannot attend mainstream education, such as vulnerable or disadvantaged groups. The Technology Ireland ICT Skillnet (ictskillnet.ie) have a broad spectrum of these types of courses, all certified and in many cases are subsidised by government. Talent shortages are being reported across all sectors, these courses provide opportunities for candidates to enrol and assess their applicability to find a new job or change career. They may also appeal to those seeking to re-join the workforce to take up employment that might have been outside their radar in the past.

M&A

In a recent report by William Fry, the TMT sector continues to be a dominant sector in terms of deal making in the first half of 2022, with 29% of the total M&A deal value and six of the 20 largest transactions. That said, total deal value was down 57% on the same period in 2021. Some of the biggest deals included Partners Group acquisition of Version 1 and JP Morgan’s acquisition of Global Shares.

Some other notable deals during the first half of the year include Ergo’s acquisition of Asystec, and DigitalWell (formerly Welltel) continuing on its acquisition journey adding IT firm ANS to expand into high-growth markets, Eleven and Wren Data, broadening the breadth and scope operationally and geographically.

TMT 2022 H2 Outlook

Technology

We expect to see a strong second half of the year as sustainability measures come into sharp focus. We anticipate that businesses across the sector are likely to see further growth and revenue opportunities. Building on initial technology transformation initiatives implemented over recent years, we will see deployment of more applications and solutions to assist in various environmental screening and energy saving initiatives. That said, vigilance will also be maintained on inflationary pressures that may have a downside impact on demand for new technologies. Suppliers will need to demonstrate the benefits of cost savings to avoid digital investments being put on hold.

Media

Global entertainment & media revenue rose by 10.4% in 2021 to US$2.34trn (PWC Global Entertainment & Media Outlook 2022 -2026 – June 2022). For many the screen industry is seen as ‘recession proof’. People will generally sacrifice socialising and discretionary costs in a recession or a downturn in the economy and will choose to stay home and watch TV or, in more recent years, stream content from various on-demand providers. The global streaming video on demand (SVoD) market is estimated to show an annual growth rate of 11.48% (Statista), resulting in a projected market volume of US$139.20bn from 2022 through 2027, with user numbers expected to grow to 1,636.0m by 2027.

Screen Ireland are already recording unprecedented growth in Ireland’s screen industry and expecting it to grow further in the current year. Many of Ireland’s animation and TV production companies refer to the ‘global insatiable demand for content’ and based on the growth projections for SVoD, it appears that Ireland looks set to benefit from this growth for the foreseeable future. Ireland may also benefit from the EU mandate that on-demand services providers must include at least 30% of the content in their catalogue that is made in Europe. The potential for the wider economy to also benefit should not be underestimated in terms of the spin-off effect for hotels and the wider hospitality and accommodation sector along with various trades and retail providers. If one reflects on the making of a major Disney blockbuster in the summer of 2021, the village of Enniskerry was transformed, where a set was built and literally hundreds of hotel rooms were filled with cast and crew over many weeks. Productions are not limited to the Dublin metropolitan area either, we can all remember Star Wars in Kerry and The Last Duel in Cahir. Every corner of Ireland has the potential to share in this growth story over the coming years.

Telecoms

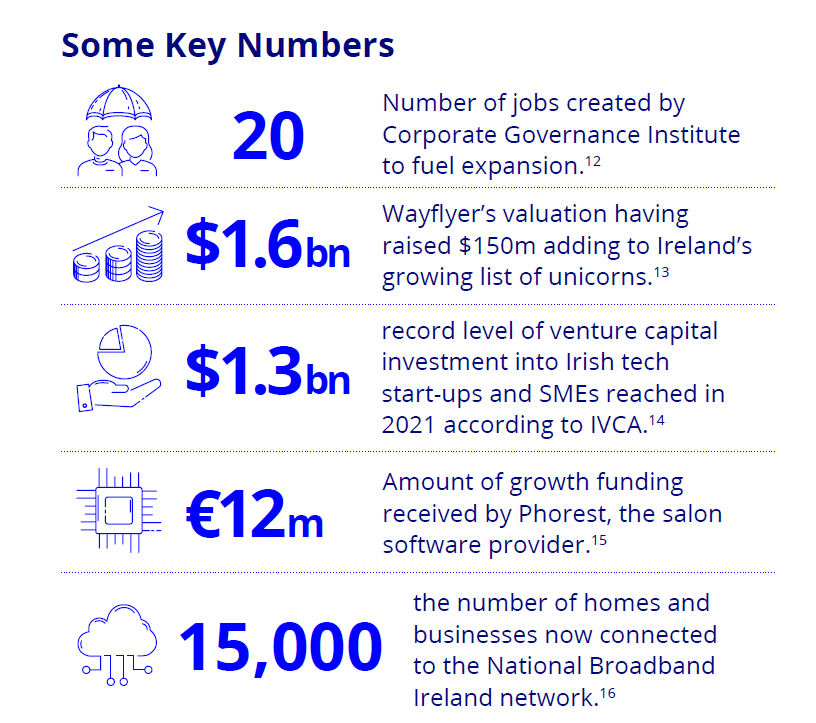

The world of work has changed, possibly forever, from what we knew before the pandemic. Remote, hybrid or teleworking, is largely dependent on good quality, stable broadband to enable people to work efficiently. National Broadband Ireland (NBI) projects that by year end 128,000 premises will be in a position to pre-order/order for broadband service with one of the providers registered on their network. Capital investment over the last five years by telecoms operators was in the region of €3.3 billion (Dept. of Env, Climate Action and Comms – May 2022) for mobile and fixed line services. This investment has greatly improved voice and data services and there is a commitment from telecoms operators to continue investment over the coming years which is estimated to be in the region of €700m.

Market

Talent shortages

The war for talent continues to be one of the major challenges right across Ireland’s TMT sectors. Remote working, depending on the business model and sector can be a blessing and a curse. There is no doubt that it has opened up opportunities to hire experienced and skilled candidates from anywhere. It has also driven up the costs of hiring for some as new candidates demand higher starting salaries than would have been the norm only a few short years ago. That said, many employers have taken a longer-term view and have chosen to pay higher salaries for skilled candidates in order to fill vacancies. From a hiring perspective the financial costs associated with hiring may have reduced by offsetting costs of travel for interviews or ultimately relocation costs once candidates are hired. Nonetheless, as the labour market continues to get tighter, there is no silver bullet to solving the shortage of talent problem.

Big tech job losses

We have seen lots of commentary and announcements of layoffs coming out of the United States in recent months. Many are speculating this is a sign of ‘big tech’ preparing for a US recession. Tesla are cutting 10% of salaried workers or 3.5%(Reuters) of their total headcount, Meta have reduced hiring of engineers by 30% (Bloomberg), Alphabet are reducing their hiring plans with new hires concentrated in engineering and other technical roles. Amazon have stated that they may have overbuilt warehouse space, expecting higher customer demand that instead waned and had hired too many warehouse workers. Given the breadth and scale of these companies, one may wonder why they are making these decisions and if they really know more about what’s coming down the line in relation to the global economy. Inflation, supply chain challenges, increase in interest rates and reversal of pandemic trends have all been mooted as potential causes. However, it is also important to note that these businesses have been on massive recruitment campaigns over the last decade and this may well be a correction in their growth journeys and making provision for the impact a recession may have, rather than a decline in demand for their products and services. Time will tell.

Consolidation across the sector

We are going to see more consolidation across the TMT sector. Technology service providers are expected to continue the same patterns of recent years, making acquisitions to broaden their geographic footprint and expand customer numbers to leverage upselling and cross selling opportunities and squeeze more revenue from their clients. Across Media we are also likely to see further investment coming into Ireland to develop new studios or acquire those already in place. Demand for live action studio space is outstripping supply so there is a ready market if the space is available. Similarly, across the telecoms sector, many of the traditional operators have sold off some of CapEx-heavy parts of their businesses, preferring to rent the real estate and infrastructure back on an operating expense basis and this may will be common trend in the time ahead.

Crypto, where is it headed?

The fall in value of both Bitcoin and Ethereum from their all-time highs in late 2021 has not been good for the crypto market. Bitcoin’s price has dropped 70% in value, having reached $68,000 last November, losing more than $2 trillion (Bitcoin Market Update – July 2022). Volatility is something that seems to go hand in hand with cryptocurrencies and those that are interested in buying into it need to be aware of this. While the value of Bitcoin has been between $22,000 and $25,000 recently, there is a lot of commentary that suggests the value will recover and may reach $100,000 at some point. Perhaps much of the mystique or attraction that still exists around the crypto market is the thrill of the chase that one could make a very hefty profit or lose it all, which feels a bit like a trip on a rollercoaster. Only with a rollercoaster, one knows where it begins and ends and when you’ll be turned upside down. We have seen over recent months a clamp down on crypto by China and President Biden signing a new executive order directing federal agencies to hone regulation on digital assets. Thus, it is probably safe to say there is yet more volatility to come.

Funding activity

Similar to recent years, digital transformation across every sector will continue to provide growth expansion opportunities for our technology customers servicing those markets. We look forward to supporting these established businesses as they look to consolidate, grow scale and their market position.

Over the last year there has been a marked increase in activity, businesses that have matured in recent years are now seeking to refinance or support MBOs/MBIs and we look forward to working with other similar businesses over the remainder of the year.

Likewise, we have supported both existing and new customers investing in their businesses to adequately resource their operations to capitalise on new opportunities and grow new markets.