Bank of Ireland head of Agriculture Eoin Lowry looks back on 2021 and outlines the key sector trends for 2022.

“The sector continues to prove its resilience and overall, the long term outlook remains positive due to continued population growth and our ability to produce high quality premium products that are globally competitive”

Excerpt:

2021 Review

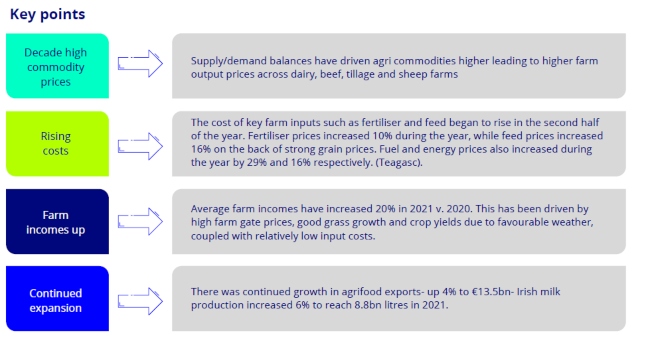

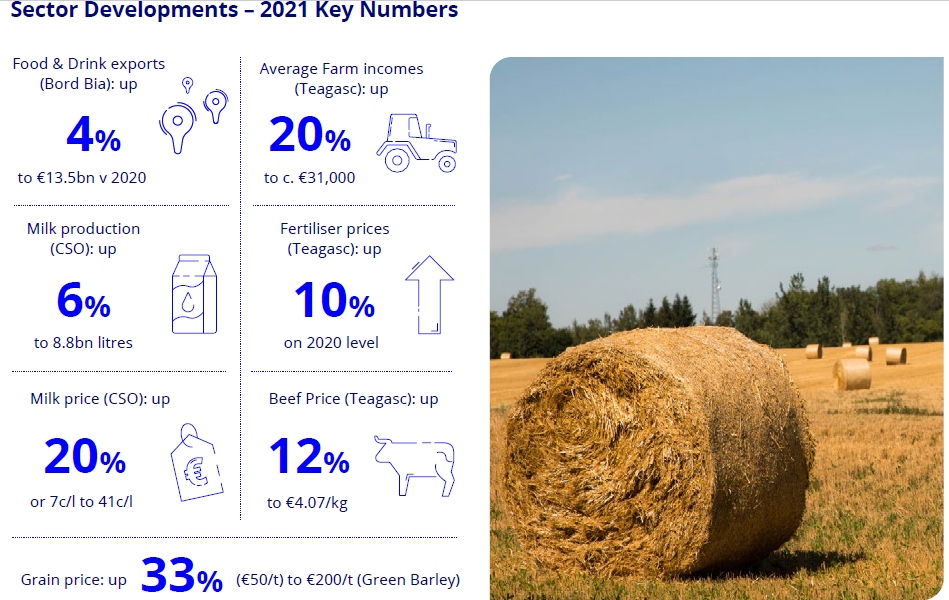

Despite the ongoing pandemic, the agri sector performed strongly in 2021. Farm incomes increased 20% in 2021 compared to 2020 driven by good weather, low input costs and decade high agri commodity prices. Brexit has had little impact with the UK still remaining the largest market for agri exports. Sentiment and investment appetite is up and farmers are coming into 2022 in a relatively strong state.

Snapshot of 2021:

Decade high agri commodity prices

The FAO Food Price Index (a measure of the change in international prices of a basket of agrifood commodities) reached a 10 year high in 2021, rising 23% over the year. For 2021, the FAO Cereal Price Index rose 27% from 2020 and is the highest annual average registered since 2012. In 2021, maize and wheat prices were 44% and 31% higher than their respective 2020 averages, mostly on strong demand and tighter supplies, especially among major wheat exporters.

The FAO Dairy Price Index rose 17% in 2021, reflecting sustained import demand throughout the year, especially from Asia, and tight exportable supplies from the leading producing regions. The FAO Meat Price Index rose 13% in 2021 with sheep meat registering the sharpest increase in prices, followed by beef and poultry, while pig meat prices fell marginally.

On the back of rising and decade high global agri commodity prices, domestic farm output prices increased with milk prices up 20% to €0.41/L, beef prices up 12% to average €4.01/kg, lamb prices up 30%, barley prices up 33%, and wheat prices up 21%. Pig prices fell 8% in 2021 as a result of local conditions (slaughtering capacity) and global factors (African Swine Flu in Germany and China).

Rising costs on farm

Total production costs increased in 2021 due to higher feed, fertiliser and fuel prices. Input usage volumes also increased in some systems. The main drivers of increased production costs included fertiliser, feed and fuel. Feed prices increased 16% on the back of strong grain prices.

Fertiliser prices increased significantly as a result of rising energy costs in the last quarter and were up 10% in 2021 v. 2020. Despite the rising costs, margins expanded across all farm systems (except for pigs) as a result of the rising global agri commodity prices that boosted farm gate prices.

Farmers continue to deleverage

The most recent data from the Central Bank shows that Irish farmers reduced their overall debt by 12% or €392m in the 12 months between September 2020 and September 2021.

Outstanding debt on Irish farms now stands at €2.8bn – its lowest level in over 10 years. At the same time, new lending to agri increased 15% or €100m in the 12 months period September 2020 to September 2021. That means that the debt on farms is getting younger and farmers are paying off debt at a faster rate than taking on new debt.

Strong sentiment on farm

Sentiment and mood is positive on farm. High prices, and relatively low costs have delivered strong cashflows with farm incomes up in 2021 v 2020. This is reflected in some key financial metrics. Bank of Ireland agri deposits have increased 10% over the past 12 months, and are now 42% higher than at the start of Covid (March 2020) understandable given that farming was deemed an essential service throughout the pandemic and was little impacted directly by Covid. Similarly, the utilization rate on overdrafts is down 10% in the past 12 months to its lowest level in 4 years.

Increased investment appetite

- Land: Given the improved profitability and strong sentiment the appetite to invest on farm and in land has increased in 2021. There was a significant improvement in the land market with more farms coming on the market in 2021. In 2020 vendors held back due to the pandemic. Indications are that the average price of land (€10,000 per acre) has increased in 2021 with some parcels where competition is high, making prices in the range €15,000-€20,000 per acre. The increase has been driven by an increase in demand, commodity prices, farm incomes, sentiment, and investors.

- Renewed Farm development: Due to the postponement of building work in 2020 as a result of Covid, farm development activity increased in 2021, driven mainly by dairy investment, along with some increases in development on tillage farms. Like other sectors of the economy, the cost of building works has increased significantly since the onset of Covid.

Little immediate impact from Brexit

One year on from the Brexit trade deal, strong commodity prices have insulated farmers from the full impact of Brexit. Beef was always expected to be the sector that would be most impacted and especially over the longer term. Given that the UK is only 75% self-sufficient in beef, its future trade policy with countries outside the EU will likely provide major exporters of meat access to its lucrative retail market. It already has concluded trade agreements with Australia and New Zealand, both major exporters of beef and sheep meat who now have enhanced access to the UK market, creating additional competition for Irish beef.

2022 Outlook

The sector continues to prove its resilience and overall, the long term outlook remains positive due to continued population growth and our ability to produce high quality premium products that are globally competitive.

The factors that will define agriculture in 2022:

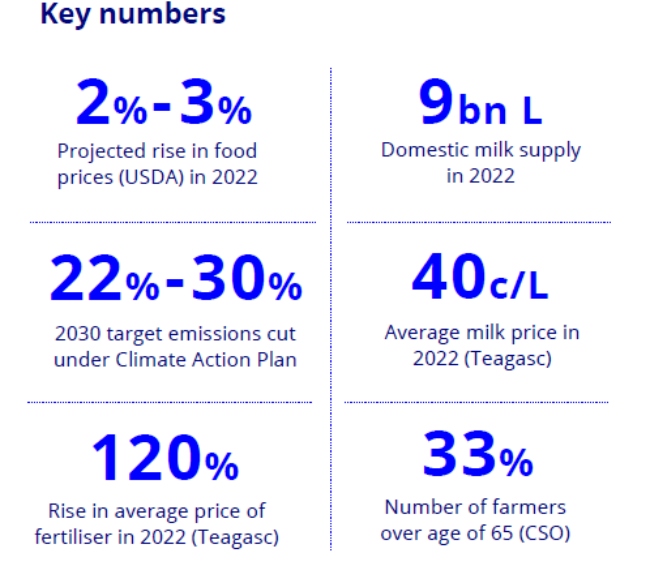

- Input price Inflation: Input costs (such as feed and fertiliser) are set to rise further in 2022 over 2021 levels, driven by increasing energy and freight costs and strong harvest 2021 grain prices. While fertiliser prices should normalise in the medium term, they are expected to peak in 2022. It is expected that fertiliser volumes will reduce 20% nationally but will be sector specific. As a result, higher volumes of feed may be used.

- Pressure on profits: In 2022, some farmers will require additional working capital to manage the increased costs and while this will squeeze margins, it is expected that farm profits will still be ahead of 2019 and 2020 figures but expected to be 20% lower on average than 2021.

- Climate Action: The Government Action Plan targets 22-30% cut in emissions from agriculture by 2030, with budgets due to be finalised in March 2022. While this is a significant reduction, the industry is confident this is achievable with minimal impact to farm output. Teagasc have stated that no cut to the national herd is needed to meet Ireland’s targets once new technologies are adopted on farms to drive efficiencies. While there will be reductions in the amount of fertiliser use permitted, there will be an increased focus on grassland management, animal breeding and organic farming practices. Additional investment such as additional slurry storage, animal housing and farm equipment will be required on farms to meet the targets.

- Evolution of the Common Agricultural Policy (CAP): The Government submitted its CAP strategic plan to the European Commission in December 2021. Further detailed engagement will take place with the Commission in the first half of 2022, with the plan expected to come into effect on 1st January 2023. Eco-payments, convergence, and limiting the maximum level of payments look set to impact every farmer. It is expected that some farmers will gain, while others will lose out as the EU aims for a fairer distribution of funds.

- Increasing role of technology on farms: Given the labour challenge on farms, there will be increased investment in technology such as automation and robotics to drive efficiency and productivity. This will also allow for improved decisions by the farmer and benefit quality of life. Technology is rapidly moving forward with advances in science driving productivity. Given the climate challenge that lies ahead technology will play a key role in addressing that challenge.

Outlook by segment

Dairy

- Production volumes are expected to increase 2-3% in 2022 due to increased cow numbers and yields.

- Current indications are that international dairy prices will remain at current levels in the short term but will decrease gradually as 2022 progresses. The outlook for 2022 is that milk prices will average c. 41c/l (Incl. VAT).

- Increased costs (feed and fertiliser) will impact margins in 2022, however incomes should remain in line with 2020 levels.

Pigs

- While the pig sector is volatile driven by supply and demand in international markets, over the commodity price cycle and in the longer term, this sector is highly efficient, productive and profitable

- Local conditions (slaughtering capacity) and global factors (African Swine Flu in Germany and China) continue to impact the pig price. However, it is expected that the pig price will improve in Q2 2022 due to a combination of reduced pig meat supply on the EU market and increased exports to China.

- The av. full year pig price for 2022 is expected to be higher than 2021 and feed prices are expected to reduce later in the year.

Beef

- Cattle prices will continue to be influenced to a large degree by the demand for Irish beef in the UK. The UK beef supply is expected to be unchanged in 2022.

- The EU beef supply is forecast to decline in 2022 which should help average Irish finished cattle prices in 2022 remain unchanged to the 2021 level of around €4/kg.

- Input expenditures in 2022 are forecast to increase on 2021 levels due to higher feed, fertiliser and energy prices.

Tillage

- While stocks to use ratios are variable across wheat, barley and maize, there remains a lot of uncertainty around grain markets. Based on current futures markets, it is expected that 2022 harvest prices may be slightly higher than those that prevailed at harvest 2021.

- Direct costs of production on cereal farms are expected to increase significantly in 2022, with key inputs such as fertiliser and seed expected to increase.

- Winter cereal area for harvest 2022 are estimated to be slightly up on 2021. Crops have been planted in good conditions.

- Boortmalt has offered grain growers a forward price of €250/t (€50/t more than January 2021) for harvest 2022.

Full report: