Ireland’s Grocery/Convenience sector continues to perform strongly, writes Owen Clifford, head of Retail Sector at Bank of Ireland. Retailers are navigating a turbulent economic environment linked to inflation, access to personnel and fluctuating consumer sentiment.

“Irish retailers are cognisant that a robust strategy for the de-carbonisation of their business model is required to meet Government, investor and consumer expectations/requirements into the future”

Retail Convenience: H1 2023 Review

Summary

- Robust performance: Robust performance delivered by the sector in H1 2023. A shift in consumer behavio

- ur to increased frequency patterns coupled with increased engagement with own-brand ranges.

- Inflation: The unprecedented level of food inflation became the subject of political focus – easing in commodity prices started to filter through to shop shelves in Q2 2023.

- Consolidation: Increased consolidation has become a feature of the market with larger grocery/fuel operators expanding their store network and diversifying their sales mix.

H1 2023 Key Trends

- Strong growth in take-home grocery sales continued. Inflation levels across the sector hit unprecedented levels (17%) linked to post Covid-19 supply and Ukraine war issues. (Kantar Grocery market share analysis Jan-June 2023)

- Dunnes continues to hold the number 1 position in respect of grocery market share driven by a particularly strong performance in the wider Dublin region. Tesco market share increased in the period reflecting the integration of the Joyce group stores within their portfolio.

- The large supermarket operators have been proactive in addressing cost of living concerns with targeted ad campaigns and voucher offers being strongly promoted. An expanded own-brand offering has also resonated with consumers with c. 16% growth delivered across unbranded lines in April/May. (Kantar grocery market share May 2023)

- Margin growth and preservation have become an imperative for retailers linked to an increased cost framework driven by personnel, insurance and energy overheads.

Key activity in the sector in 2023

Shopping patterns reflected cost of living concerns with increased frequency (shopping little & often) becoming a feature of the market. The normalisation of food inflation, linked to a significant decline in international food commodity prices in recent months, (based on historical evidence, food retail prices adjust to changes in commodity prices with a time lag of about six to twelve months) will be monitored closely in H2 2023.

Retailers are continuing to implement pragmatic succession planning structures to ensure that appropriate long-term value is delivered from their business. COVID-19 has been a catalyst for some retailers to investigate future options in respect of both ownership and operational models.

Recent studies across Europe have demonstrated that saving money on food remains a top priority across all income groups. This has led to increased engagement with own brand products and a discernible improvement in own-brand range/options across the sector. The proactive delivery of premium, healthy and sustainable products across the own-brand range will be required to meet customer expectations and preserve retailer margins. (McKinsey, grocery trends 2023)

Sector Developments:

Investment & Economic

- Supervalu, Lidl, Aldi, Tesco and Dunnes all announced new store openings/significant store revamps in H1 2023 across all regions supporting job creation and the wider Irish business eco-system.

- The increased cost and regulatory burden presented by the proposed living wage structure, pension auto-enrolment and insurance in a competitive environment has led to an up weighted focus on margin development/preservation from retailers, wholesalers and their advisors. Access and retention of personnel in a “full-employment” environment continues to be a key challenge for the sector.

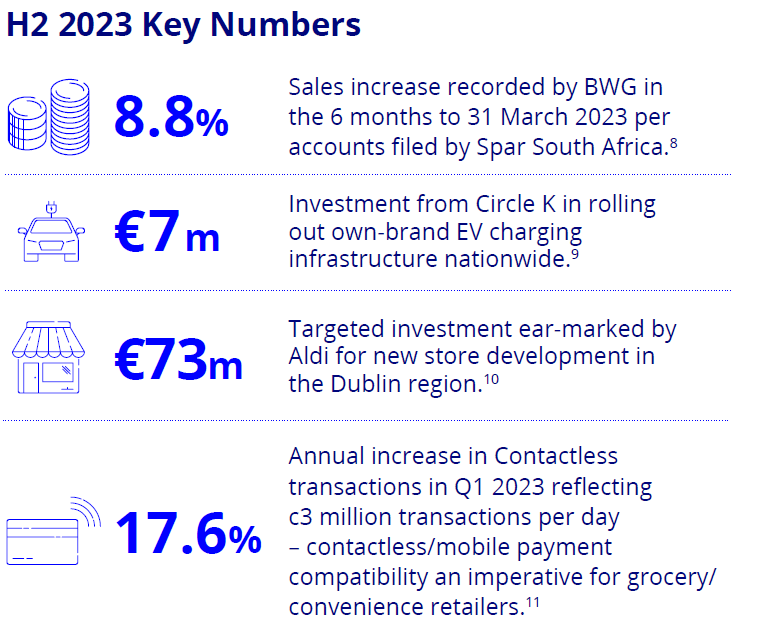

- Consolidation and cross-sectoral partnerships remains a feature of the wider Irish grocery/convenience/forecourt market. Tesco integrating nine Joyce group stores within their network, BWG agreeing terms to purchase Tuffy wholesale and Corrib Oil expanding their store portfolio nationwide a flavour of some of the transaction activity in H1 2023.

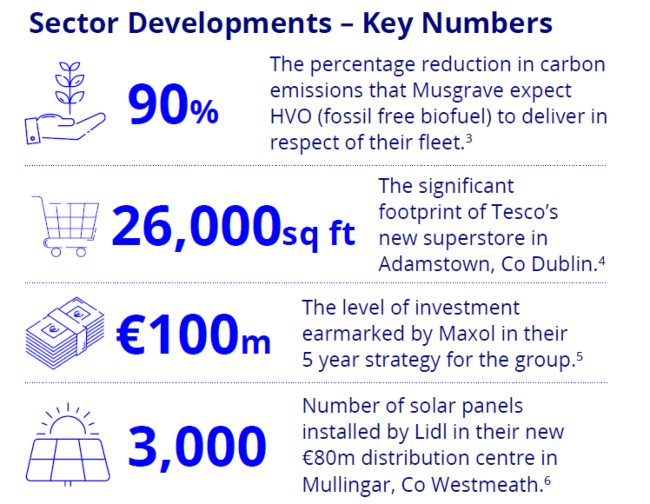

- The de-carbonisation of end to end operations remains a key focus for leading operators linked to supplier, Government and consumer expectations/requirements. Multi-million euro investments linked to improving energy efficiency profile across the fleet, logistics and store network was a feature of sector announcements/strategies in H1 2023. The requirements of international suppliers seeking to reduce their scope 3 emission profile will continue to act as a driver/incentive in the green transition of the Irish grocery/convenience sector.

H2 2023 Retail Convenience outlook

- Robust Outlook: Overall a resilient sector to economic shocks; Strong sales performance to continue but increased focus on margin preservation and cost management required to maintain profitability levels/leeway for investment.

- Funding Activity: Strong active pipeline of store purchase and associated revamp proposals– retailers recognise that customer experience/excellent standards will be key to attract and retain market share.

- ESG Investment: Increased investment in environmentally focused store network, waste management, circular operational framework and fleet fuel consumption to support targeted reduction in carbon emissions from the sector.

Market

- In a competitive labour market – sourcing and retaining the best people is vital to sustain a retail business. A structured employee development plan that incorporates role variety, up-skill opportunities and competitive remuneration needs to be embedded within the culture of the business. The smart use of digital/automation tools can deliver the dual goal of increased efficiency and an improved working environment.

- Consistent with the wider European model, the digital transformation of the Irish grocery sector has been fragmented to date leading to cost/operational inefficiencies and delays in the delivery of improved supply chain, analytics and omnichannel models across the sector.

- Retailers recognise that appropriate investment in this area is a key step in preserving profitability – ensuring that investment can be continued in the traditional areas of personnel, store design and product offering

- Significant revamp programmes will continue to be rolled out in 2023 nationwide by leading grocery operators as the ever more discerning consumer seeks excellence in store standards. Movement on revamp costs linked to fluctuating material supply base to be monitored closely.

- Detailed analysis pre and post revamp will be an imperative to ensure that a maximum return on investment is delivered via sales mix improvement, margin growth and cost saving.

- The “localisation” trend will continue with store revamps taking a more bespoke, community focused approach

- Consolidation is expected to remain a feature of the market with wholesalers, fuel brands and multi-store retailers expanding their network and footprint across the sector

- As consumers seek cheaper alternatives across some product lines, all leading operators recognise that a strong, diversified own-brand offering will be critical to maintain customer engagement as the inflationary cycle continues.

Environmental, Social & Governance (“ESG”)

- Irish retailers are cognisant that a robust strategy for the de-carbonisation of their business model is required to meet Government, investor and consumer expectations/ requirements into the future. Corporate social responsibility linked to sustainable and environmentally friendly in-store activities will therefore be a key area of focus for all retailers

- Energy efficient equipment, elimination of single-use plastic, improved recycling facilities and reduction of food waste. This will enable an improved cost base whilst meeting consumer expectations in respect of ethical trading. The proposed roll-out of the deposit return scheme will be monitored with interest.

- Studies have identified that c90% of all emissions related to Retail are Scope 3 – linked to suppliers/consumers as opposed to direct emissions from the business itself/purchased energy (Scope 1 and 2). To move the dial on Scope 3, retailers are starting to establish joint initiatives and incentivisation plans with their suppliers to support improved emission targets and the sharing of related data. In respect of consumer engagement – apps/tools that support customers to set and monitor climate targets for their shopping baskets are also on the horizon.

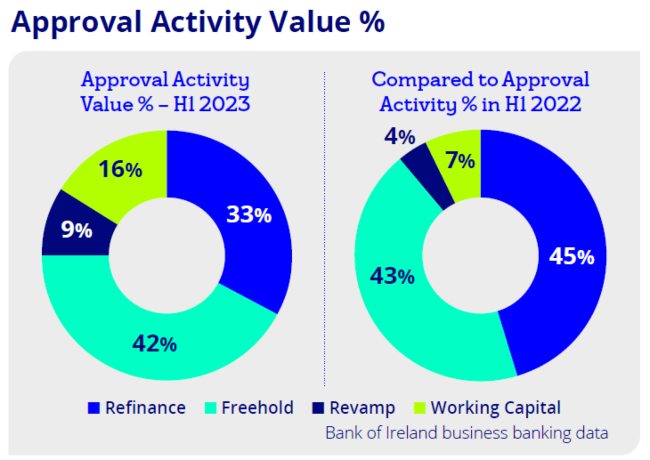

Funding Activity

- Store purchase strategies will continue to develop in 2023. COVID-19 has been the catalyst for increased levels of succession planning/retirement which is driving this activity.

- Revamp funding to continue with a particular focus on energy efficient equipment and processes.

- Robust refinance activity projected linked to loan book purchasers seeking to deleverage.